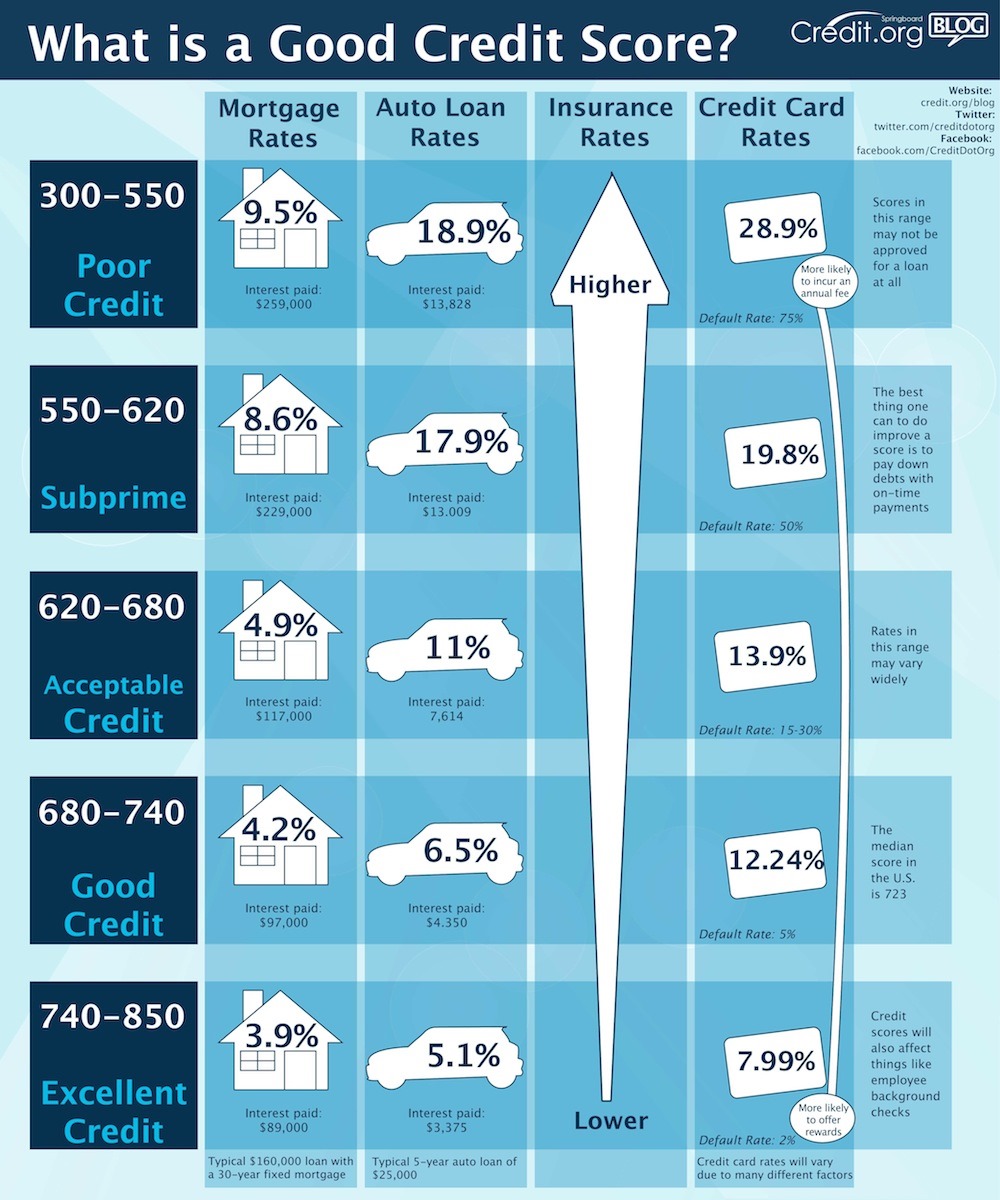

Credit scoring is a strategy of deciding the chance that credit end users will pay their charges. Truthful, Isaac started its function with credit scoring in the late fifties and, given that then, scoring has become commonly recognized by loan providers as a dependable signifies of credit evaluation. A credit score attempts to condense a borrower’s credit heritage into a solitary number. Honest, Isaac & Co. and the credit bureaus do not reveal how these scores are computed. The Federal Trade Fee has ruled this to be satisfactory.

Isn’t it intriguing that the score most crucial in our economic life, our customer credit score does not even include full disclosure? As mentioned previously mentioned the Federal Trade Fee has ruled that it is alright for Truthful Isaac & Co not to disclose the algorithms used in this method, but what about consumer legal rights. Although it is important to understand what a FICO rating is, it is not the primary situation of this paper, insurance costs are. So the place is the link? All the general public is aware of is that Fair Isaac tells us there is a substantial correlation amongst folks with undesirable credit and substantial risk motorists. This notion is crazy and from what I can see from this black box strategy, there is no genuine causation in between the two. This sort of reasoning is related to convicting a person of anything ahead of they have even committed a criminal offense. For instance, let’s say I do a study and that research displays there is a substantial correlation among criminals and men and women with negative credit. Is this to say that just since you have negative credit you are far more likely to dedicate a crime and therefore you need to be profiled or possibly locked up due to the fact you are a threat to society?

This system is discriminating towards minorities, disabled and in my scenario college students among other individuals. Truthful Isaac & Co statements that they cannot demonstrate the innovative algorithms they use to determine these correlations and scores simply because they dread that they would be offering up beneficial proprietary details that was really high priced to produce and preserve. What about the cost to consumer’s who may possibly be having to pay increased charges or in even worse cases even denied insurance coverage primarily based on these procedures.

The Equivalent Credit Opportunity Act forbids lenders from considering race, sexual intercourse, marital status, countrywide origin, and faith, but if we don’t even know how these organizations are calculating these scores, how in the entire world could we perhaps know whether or not or not they are discriminating. This smoke and mirror method is what several authorities agencies do to subtly discriminate and extort money from the American.

What about extortion? As I replicate on this topic extortion comes to thoughts. Webster defines extortion as to “obtain by drive or compulsion.” By employing such unfounded tactics shoppers are compelled into having to pay the greater costs. Initial of all, ninety% of all insurance policies companies use this procedure secondly in the interest of society legislation calls for all People in america with automobiles to have auto insurance policies. Dwelling in a nation in which it is virtually impossible to reside with no a vehicle does not this existing some force to pay out the costs? Also, allows say you are not able to afford to get a car with cash, in which circumstance you could obtain liability insurance policies alone and help save quite a good deal of money but as an alternative you just take out a financial loan, the financial institution will need you to get total protection auto insurance coverage to cover them until you spend off the financial loan. While this case may possibly not represent an severe scenario of extortion it does give purpose to ponder the connection.

Insurance firms tout on their own as symbolizing peace of brain, safety and security, but at what expense. Over the past ten several years, I have invested approximately 20,000 pounds in car insurance policy, what have I claimed? Effortlessly considerably less than 50 % and I totaled a automobile. Is insurance policy just a type of legalized gambling protected by authorities? The McCarran-Ferguson Act of 1944 exempts the insurance policies sector from antitrust laws, so listed here we are again without a selection collusion is the rule not competitiveness. Where are the ethics of lawmakers? Several states are screaming about this controversial situation and some states this sort of as California have experienced some success, but with security from best authorities what can customers do?

I have individually created the Governor of Pennsylvania about the subject, one particular of my main concerns was

“I am a anxious citizen. Recently I observed my car insurance policy prices escalating at a significant fee. I investigated the predicament only to uncover out that my credit score was creating the variation, not my driving report.”

The response I received from the Section of Insurance coverage follows:

This letter is in reponse to your criticism filed with the Pennsylvania Insurance policy Dpartment through Governor Edward G. Rendell's correspondence office relating to the use of credit as an underwriting device for vehicle insurance policies in Pennsylvania.

I have study through your issues and it seems that you are questioning the underwriting of vehicle insurance. Particularly, the use of credit in determining eligibility. Several various elements go into the underwriting of an insurance policy plan, this kind of as type of automobile, motorists, place, etc. and most recently credit history. Pennsylvania legislation does not prohibit an insurance coverage organization fromusing credit as an underwriting device so lengthy as it is done within the very first 60 days of producing a plan. Below tra cứu thông tin doanh nghiệp , an insurance business is granted a 60 day window from the inception of a plan to figure out regardless of whether or not the plan matches into the firm's suggestions.

In your letter, you stated credit scoring in element of the ranking structure and presumable should be authorized by the Insurance Office. Actually, credit scoring is part of a company's underwriting guidelines and the Dapartment only regulates underwriting guideline to the extent they are not discriminatory.

Also, Federal law beneath the Reasonable Credit Reporting Act enables credit details to be used for underwriting monetary and insurance policy transactions.